Editor’s Note: The topline metrics referenced in this article are drawn from the D-Tools 2025 Year-in-Review Report, which analyzes proposal and signed-contract data from D-Tools Cloud users across both residential and commercial integration markets. The methodology differs from NSCA’s Financial Analysis of the Industry (FAI) report, which is based on contractor financial statements and broader cost-of-doing-business accounting practices. In particular, labor burdening and cost allocation methodologies may vary among D-Tools users, which can impact reported gross margin figures. As a result, certain metrics—especially gross margin—may not align directly with NSCA benchmarking data and should not be viewed as apples-to-apples comparisons.

Systems integrators averaged 18.8% sales growth last year, driven by steady demand across several market sectors. Specifically, the average integrator signed 75 contracts worth $13,739 each. Compared to 2024, this represents:

- A 13% increase in contract volume

- A 5.2% rise in average contract value

These are just a few of the topline numbers from D-Tools’ recently released 2025 Year-in-Review Report, which is available as a free download. On its face, the industry looks healthy, but a more complicated picture emerges when you look closer.

One in five integration companies saw revenues decline by 21% or more in 2025. At the same time, 35% of integrators posted revenue growth of 51% or more. It’s the same market, but integrators are experiencing very different outcomes. The market isn’t rising evenly—it’s splitting. And that split cuts across every company size, from small companies to large firms.

Profit Takes a Slight Hit

Making the picture more difficult is what happened to profitability. Gross margins fell from 41.9% in 2024 to 38.6% in 2025, a drop that deserves attention.

The cause can be traced back to the composition of integrator revenue: 76% of installation contract revenue is tied to equipment and 24% is tied to labor. That exposes integrators to swings in equipment price, which is exactly what happened in 2025.

Equipment prices spiked as the result of tariff pressures and supply chain disruptions. The 5.2% rise in average contract value sounds positive until you consider that it was more than double the general U.S. inflation rate of 2.7% for the year. Integrators were likely raising prices to cover rising costs.

The integrators that couldn’t pass those costs through to customers absorbed the hit in their margins. For example, most probably couldn’t adjust their pricing to accommodate the topsy-turvy tariffs on projects they had mid-pipeline, so the result was more revenue on paper but less money kept.

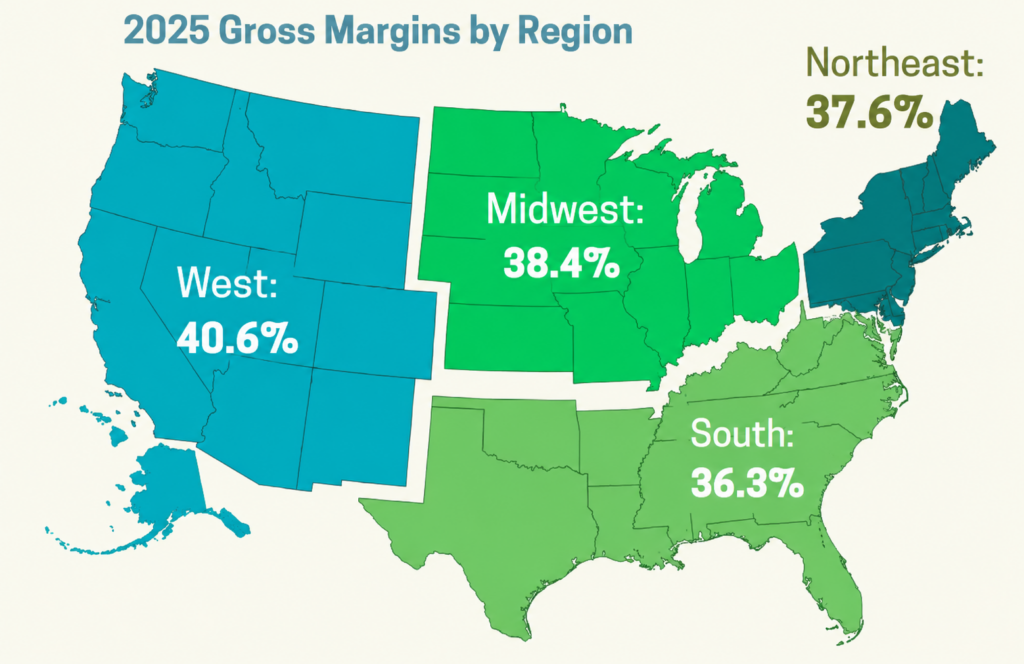

Regional Differences Are Real

Regional dynamics add another layer of complexity. Integrators in the West posted the highest gross margins at 40.6%, while those in the South came in at just 36.3%.

But regional margin differences aren’t explained by labor rates. For example, the Northeast commands the highest hourly labor rates in the country at $400 per hour (vs. $169 in the South). But these higher labor billing rates don’t automatically translate to better margins when the cost structure beneath them is just as elevated. Taxes, insurance, wages, and logistics all contribute to higher operating costs in those regions.

Project scale tells a different story. Mean project values in the West reached $18,917, compared to $12,925 in the Midwest. This suggests that regional market conditions and commercial construction activity are shaping outcomes as much as anything a company does internally.

Vertical Market Focuses Are Contrasting

Vertical market exposure matters, too. D-Tools data shows that growth for commercial integrators outpaced residential-focused integrator growth by 1.6x more in 2025.

Commercial integrators that diversified into corporate, education, government, hospitality, and/or retail were positioned to capture that faster-growing segment. Those that remained heavily concentrated in residential—particularly in markets where high-end new construction slowed—had fewer tailwinds working in their favor.

Operational Execution Matters

Another factor to consider in the performance gap is sales execution, which may be the most controllable variable of all.

The national close rate in 2025 was 69.7%. But integrators that delivered proposals within 48 hours of a site visit or client meeting closed at 88%, nearly 19 percentage points higher. Speed signals competence and reduces the window in which a prospect shops competitors. It also reflects an operational discipline that tends to run through everything else a well-run firm does.

Moving into the Growth Cohort

So, what separates the high-performing integrators from those that are falling behind? The answer is rarely a single factor: It’s the combination of diversified vertical market exposure, tight operational cost management, strong proposal processes, and the ability to use data—not instinct—to run the business.

Companies that want to move into the growth cohort should start by fully leveraging their business management software to track margins by

- Job type

- Technician

- Geography

An outside consultant’s assessment of workflow and profitability can surface blind spots that are invisible from the inside. Proposal speed must become a cultural and operational priority, not an afterthought. And as AI-driven discovery increasingly shapes how buyers find service providers, firms need a web presence and content strategy built for how clients search today, not how they did five years ago.

The market grew. But growth without margin improvement is a warning sign, not a celebration. The integrators that understand the distinction are the ones that will still be talking about growth five years from now.

D-Tools is an NSCA Business Accelerator.

*Editor’s Note: The topline metrics referenced in this article are drawn from the D-Tools 2025 Year-in-Review Report, which analyzes proposal and signed-contract data from D-Tools Cloud users across both residential and commercial integration markets. Because the methodology differs from NSCA’s Financial Analysis of the Industry (FAI) report—which is based on contractor financial statements and broader cost-of-doing-business accounting practices—certain metrics, including gross margin, may not align directly with NSCA benchmarking data. Readers should avoid making direct apples-to-apples comparisons between the two reports without considering those methodological differences.